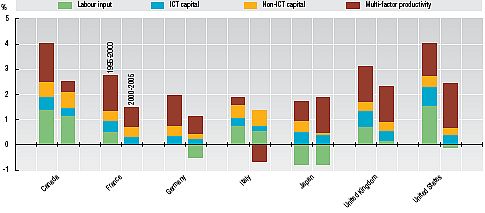

I had previously written that “the (new) service economy is not the same as the service sector“. There’s an deep problem in trying to define and measure something new, when we have to rely on government statistics that have an anchor point of 1980, 1971, or even 1945. Using old definitions doesn’t necessary invalidate the measurements, but is problem if we’re dealing with a paradigm shift in a scientific revolution.

In quantifying economic systems, many of the approaches take an output-oriented (i.e. GDP or value-added) approach. Another alternative is to take an input-oriented approach (i.e. labour). Looking into labour has brought me back to Richard Florida’s research. In The Rise of the Creative Class (2002) appears a breakdown of U.S. statistics that contrast to the three-sector view.

Appendix Table 1 Counting the Classes, 1999 [p. 330]1

Share Employees (OES data) Percent Share Employees (Emp. & Earnings data) Percent Share Creative Class 38,278,110 30.0% 38,453,000 28.8% Super-Creative Core 14.932,420 11.7% 14,133,000 10.6% Other Creative Class 23.345,690 18.3% 24,320,000 18.2% Working Class 33,238,810 26.1% 32.760,000 24.5% Service Class 55,293,720 43.4% 58,837,000 44.1% Agriculture 463,360 0.4% 3,426,000 2.6% Total 127,274,000 133,488,000

Why does the view of occupations as super-creative core and other creative class matter? From The Flight of the Creative Class in 2004, creative class occupations are shown to drive disproportionate amounts of wealth generation in the U.S. (Their creative sector I’ll frame as “new” service economy occupations, to contrast from their service sector as traditional service economy occupations).

I had previously written that “the (new) service economy is not the same as the service sector“. There’s an deep problem in trying to define and measure something new, when we have to rely on government statistics that have an anchor point of 1980, 1971, or even 1945. Using old definitions doesn’t necessary invalidate the measurements, but is problem if we’re dealing with a paradigm shift in a scientific revolution.

In quantifying economic systems, many of the approaches take an output-oriented (i.e. GDP or value-added) approach. Another alternative is to take an input-oriented approach (i.e. labour). Looking into labour has brought me back to Richard Florida’s research. In The Rise of the Creative Class (2002) appears a breakdown of U.S. statistics that contrast to the three-sector view.

Appendix Table 1 Counting the Classes, 1999 [p. 330]1

Share Employees (OES data) Percent Share Employees (Emp. & Earnings data) Percent Share Creative Class 38,278,110 30.0% 38,453,000 28.8% Super-Creative Core 14.932,420 11.7% 14,133,000 10.6% Other Creative Class 23.345,690 18.3% 24,320,000 18.2% Working Class 33,238,810 26.1% 32.760,000 24.5% Service Class 55,293,720 43.4% 58,837,000 44.1% Agriculture 463,360 0.4% 3,426,000 2.6% Total 127,274,000 133,488,000

Why does the view of occupations as super-creative core and other creative class matter? From The Flight of the Creative Class in 2004, creative class occupations are shown to drive disproportionate amounts of wealth generation in the U.S. (Their creative sector I’ll frame as “new” service economy occupations, to contrast from their service sector as traditional service economy occupations).